'Tracing the Origins of the Netherlands' Tax Treaty Network'

M. Evers LL.M. - Intertax 2013-6/7 (Download through SSRN)

'De relatie met Duitsland en de geboorte van het Nederlandse fiscale verdragsbeleid'

M. Evers LL.M. - WFR 2012/501

Summary

In 2012 and 2013, Evers analysed the historical background of the conception of the tax treaty network of the Netherlands. Archival research resulted in two publications on this subject. In April 2012, the Dutch tax law review Weekblad Fiscaal Recht published 'De relatie met Duitsland en de geboorte van het Nederlandse fiscale verdragsbeleid'. An adapted and elaborated version of this publication was published in the 2013 Summer issue of Intertax. Outcomes of Evers' research were also presented on various international conferences. The presentation can be found in a seperate post on this weblog.

Summary

Evers analysed the economical and political background of the early agreements on trade and taxation between Germany and the Netherlands. Clashes between dominant states such as France, Prussia and Austria determined the political landscape of 19th century Northern Europe. These clashes had a great impact on smaller neighbouring countries such as the Netherlands and Belgium. German states meanwhile went through a proces of integration and unification. In this proces, taxes played an important role. During this time, the first agreements for the avoidance of double taxation were developed. This also means that the foundations for the current international tax system were laid long before the League of Nations committees had begun their work in international tax law. Consequently, the roots of instruments used for Base Erosion and Profit Shifting (BEPS) can be tracked down to 19th century continental Europe.

(Click 'read more' to continue reading)

The first negotations between the Netherlands and Germany started in 1904 as a result of complaints of an influencial double tax resident: Count William Bentinck von Waldeck und Limpurg. His complaint sparked internal debate among Dutch bureaucrats and prompted the development of instruments for the avoidance of double taxation, while Dutch income taxation was being developed in 1905-1914. As became clear by research of the author, it was already during WWI that the Netherlands envisaged to become a linking pin in international taxation. The Netherlands legislator therefore adjusted the Netherlands tax system to provide for a basis of fruitful international tax policies.

Meanwhile, the Netherlands tried to enter into negotations with Germany regarding a treaty for the avoidance of double taxations. Actual negotiations took off after WWI. Between 1920 and 1928 the countries corresponded on draft treaty texts. For Germany, the main negotiator was Herbert Dorn. The Dutch head of delegation was Sinninghe Damsté. Both were Directors of Taxation for the Ministries of Finance of their respective countries.

A few years later, both Dorn and Sinnighe Damsté joined the League of Nations Tax Committees. Their experience from the bilateral negotiations between Germany and the Netherlands must have influenced their committee work.

The first treaty between Germany and the Netherlands was signed in 1928. This treaty, however, was never published or ratified. In the contribution in Weekblad Fiscaal Recht, Evers uncovers the reasons why it would take another three decades, before a treaty between the two neighbouring countries would be ratified.

Background Information

The research conducted for this contribution uncovered a collection of historical documents. Some of these documents can be found by opening the full text of this weblog post (click on the title).

Documents

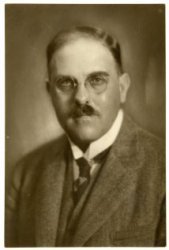

One of the key persons in early Dutch international tax policy was J.H.R. Sinninghe Damsté. For years, he was Director of Taxation of the Netherlands Ministry of Finance. He was mandated to negotiate on the Netherlands first DTA: a DTA with Germany. During the ratification of the 1928 tax treaty between the Netherlands and Germany, it turned out that the Alleingang of Sinninghe Damsté had been a big risk.

Sinninghe Damsté's early experiences as a tax treaty negotiator must have influenced the work of the tax committees of the League of Nations. Together with his German counterpart, Sinnighe Damsté was an important contributor to the work of these committees.

Herbert Dorn

Dorn was Director of Taxation for the Ministry of Finance in pre-WWII Germany. Dorn and Sinnighe Damsté negotiated on a DTA between Germany and the Netherlands in the early 1920s. Dorn became Justice in the German Finanzhof, before the Nazi Government introduced legislation limiting the professional activities of persons with a Jewish background. Dorn, Jewish himself, fled to Cuba and later the USA via Switzerland before WWII started.

More information on Dorn can be found in this brochure of the German Ministry of Finance: link.

Dorn was Director of Taxation for the Ministry of Finance in pre-WWII Germany. Dorn and Sinnighe Damsté negotiated on a DTA between Germany and the Netherlands in the early 1920s. Dorn became Justice in the German Finanzhof, before the Nazi Government introduced legislation limiting the professional activities of persons with a Jewish background. Dorn, Jewish himself, fled to Cuba and later the USA via Switzerland before WWII started.

More information on Dorn can be found in this brochure of the German Ministry of Finance: link.

William Bentinck Waldeck-Limpurg (two generations)

The Bentincks sparked Netherlands tax treaty policy, as was uncovered by Evers's research. This family of noblemen had premises in both the Netherlands and Germany. The German family estates were located in current Baden-Würtemberg, around the village of Gaildorf.

The Dutch family Castle Middachten is located in Gelderland. In 2011, William's daughter received an award for the renovations to the castle. In a video made for the occasion of the award ceremony, she refers to the tax issues that forced the family to move to Germany permanently in 1929.

M. Evers LL.M. - Intertax 2013-6/7 (Download through SSRN)

'De relatie met Duitsland en de geboorte van het Nederlandse fiscale verdragsbeleid'

M. Evers LL.M. - WFR 2012/501

Summary

In 2012 and 2013, Evers analysed the historical background of the conception of the tax treaty network of the Netherlands. Archival research resulted in two publications on this subject. In April 2012, the Dutch tax law review Weekblad Fiscaal Recht published 'De relatie met Duitsland en de geboorte van het Nederlandse fiscale verdragsbeleid'. An adapted and elaborated version of this publication was published in the 2013 Summer issue of Intertax. Outcomes of Evers' research were also presented on various international conferences. The presentation can be found in a seperate post on this weblog.

Summary

|

| One of the double resident's homes |

(Click 'read more' to continue reading)

The first negotations between the Netherlands and Germany started in 1904 as a result of complaints of an influencial double tax resident: Count William Bentinck von Waldeck und Limpurg. His complaint sparked internal debate among Dutch bureaucrats and prompted the development of instruments for the avoidance of double taxation, while Dutch income taxation was being developed in 1905-1914. As became clear by research of the author, it was already during WWI that the Netherlands envisaged to become a linking pin in international taxation. The Netherlands legislator therefore adjusted the Netherlands tax system to provide for a basis of fruitful international tax policies.

|

| Sinninghe Damsté |

A few years later, both Dorn and Sinnighe Damsté joined the League of Nations Tax Committees. Their experience from the bilateral negotiations between Germany and the Netherlands must have influenced their committee work.

The first treaty between Germany and the Netherlands was signed in 1928. This treaty, however, was never published or ratified. In the contribution in Weekblad Fiscaal Recht, Evers uncovers the reasons why it would take another three decades, before a treaty between the two neighbouring countries would be ratified.

Background Information

The research conducted for this contribution uncovered a collection of historical documents. Some of these documents can be found by opening the full text of this weblog post (click on the title).

Documents

- F.T. Ploeckl, ‘The Zollverein and the formation of a customs union’, discussion Papers in Economic and Social History nr. 84, August 2010 (analysing the formation process of the German Zollverein).

- Overeenkomst inzake de wisseling van renvooien tussen de Nederlandsche en Belgische administratie van 24 mei 1845 (still existing mutual assistance treaty between Belgium and the Netherlands (in Dutch))

- R. Arndt (red.),

- Die Reden des Grafen von Caprivi, Hamburg Severus 2011, (speechers of German Kanzler Caprivi, including the phrase “Wenn ich jemand wirtschaftlich mit einem Krieg überziehe, so will ich ihn schwächen; wir aber haben gerade das Interesse, unsere Verbündeten zu stärken’”)

- Draft of first Netherlands Income Tax Act, including reference to avoidance of double taxation: Kamerstukken II 1907/08 nr. 98 (Dutch)

- Double taxation and Tax Evasion, Report presented by the General Meeting of Government Experts on Double Taxation and Tax Evasion, Genève: Volkenbond 1928 (Publications of the League of Nations 1928.II.49).

- Netherlands Government planned to develop the Netherlands into a conduit jurisdiction during the First World War (Dutch

- Memorie van Toelichting bij Grondslagen van het stelsel van ’s Rijks belastingen, Bijlagen Kamerstukken II 1915/16, nr. 198, ondernummer 3)

- Open this link for various documents, including;

- The first DTA between Prussia and Sachsen of 16 December 1869

- The Reichs Law for the avoidance of double taxation of 18 July 1871

- Various Tax Reports of the League of Nations

Persons

Sinninghe DamstéOne of the key persons in early Dutch international tax policy was J.H.R. Sinninghe Damsté. For years, he was Director of Taxation of the Netherlands Ministry of Finance. He was mandated to negotiate on the Netherlands first DTA: a DTA with Germany. During the ratification of the 1928 tax treaty between the Netherlands and Germany, it turned out that the Alleingang of Sinninghe Damsté had been a big risk.

Sinninghe Damsté's early experiences as a tax treaty negotiator must have influenced the work of the tax committees of the League of Nations. Together with his German counterpart, Sinnighe Damsté was an important contributor to the work of these committees.

Herbert Dorn

Dorn was Director of Taxation for the Ministry of Finance in pre-WWII Germany. Dorn and Sinnighe Damsté negotiated on a DTA between Germany and the Netherlands in the early 1920s. Dorn became Justice in the German Finanzhof, before the Nazi Government introduced legislation limiting the professional activities of persons with a Jewish background. Dorn, Jewish himself, fled to Cuba and later the USA via Switzerland before WWII started.

Dorn was Director of Taxation for the Ministry of Finance in pre-WWII Germany. Dorn and Sinnighe Damsté negotiated on a DTA between Germany and the Netherlands in the early 1920s. Dorn became Justice in the German Finanzhof, before the Nazi Government introduced legislation limiting the professional activities of persons with a Jewish background. Dorn, Jewish himself, fled to Cuba and later the USA via Switzerland before WWII started. William Bentinck Waldeck-Limpurg (two generations)

The Bentincks sparked Netherlands tax treaty policy, as was uncovered by Evers's research. This family of noblemen had premises in both the Netherlands and Germany. The German family estates were located in current Baden-Würtemberg, around the village of Gaildorf.

The Dutch family Castle Middachten is located in Gelderland. In 2011, William's daughter received an award for the renovations to the castle. In a video made for the occasion of the award ceremony, she refers to the tax issues that forced the family to move to Germany permanently in 1929.

No comments:

Post a Comment